I'm Tom Wheelwright, CPA

Entrepreneur, Best Selling Author, Rich Dad Advisor® & International Authority on Tax

“My goal in life is to make taxes fun, easy & understandable!”

The Truth About Taxes

The tax law is a roadmap to financial freedom, filled with incentives for entrepreneurs and investors! You just have to follow the rules of the rich!

Wealth Through Taxes

Taxes are looked at so negatively by most people, but taxation is actually one of the most powerful tools for wealth creation!

Start With Your Dream

Identify The Goal

Create The Team

Implement The Strategy

About Tom

Tom Wheelwright, CPA is the visionary and best selling author behind multiple companies that specialize in wealth and tax strategy. Tom is also a leading expert and published author on partnerships and corporation tax strategies, a well-known platform speaker and a wealth education innovator.

Published Professional

Tom is a regular commentator in the field of taxes and contributes regularly in major professional journals and online resources. Tom’s work has been featured in hundreds of media, including Forbes, The Huffington Post, Accounting Today, CFO Magazine, ABC News Radio and AZTV Morning News, along with writing columns for Entrepreneur Magazine and Inman News.

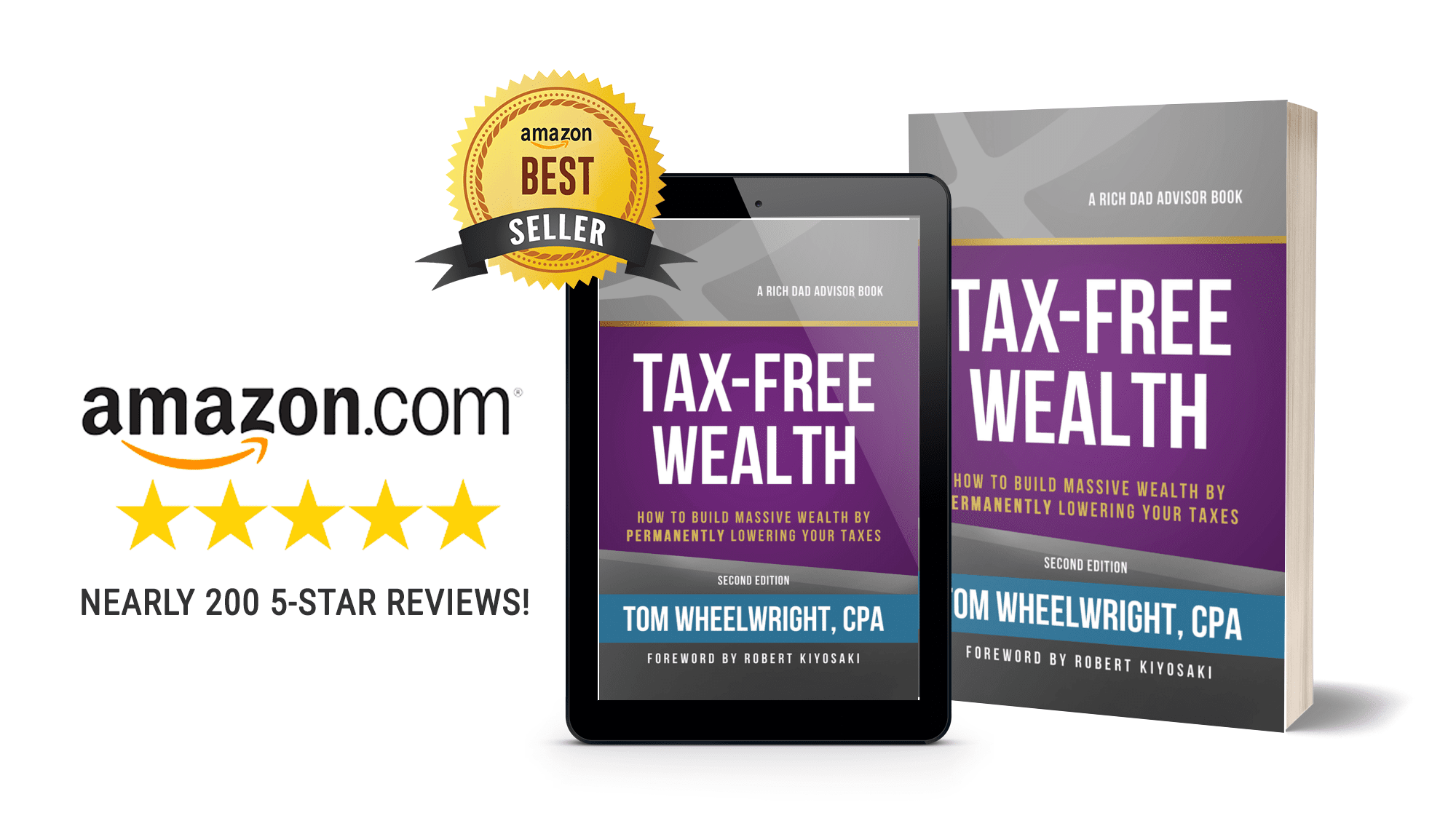

Best Selling Author

In Tom’s best selling book Tax-Free Wealth, Tom shows entrepreneurs and investors how to build massive amounts of wealth through practical and strategic ways to permanently reduce taxes

Finally! A tax book that lifts the veil for everyone!

My tax preparer was very impressed with the book. She knew some of the strategies in the book because she does them for her wealthiest clients. But, it never occurred to her that they also work for the working middle class who are looking to move upwards financially. I am very enthusiastic about the positive changes I am making in my financial life.

Never thought taxes could make me want to earn more money!

Taxes rarely excite anyone. Tax-Free Wealth actually got me pumped with ideas on how my family could make more money and pay less taxes. While the tips and secrets aren't for everyone, those with an entrepreneurial spirit will get pumped about Tax-Free Wealth. If you work for someone else and aren't interested in real estate, investing, or owning your own company, don't waste your money – this book is not for you.

Finally, the “Rich Dad” Principles Are Clear

If you are a fan (or student) of the “Rich Dad, Poor Dad” series, and understand those basic principles, but may feel as if you are still missing a piece of the puzzle toward building wealth—-then you must read this book. This book will fill that void.

This book ties all the Rich Dad principles together and demonstrates how and why they work to build vast wealth over a lifetime—and beyond—for generations to come. I truly understand now why the old adage of “the rich just keep getting richer” is so true: the tax code.

Contributing Author

Tom has contributed to a number of books. Including The Real Book of Real Estate (December 2016), Tom was the author of Chapters 1 and 21. Tom also contributed to Robert Kiyosaki's Rich Dad Success Stories (2003), Who Took My Money (2004), Unfair Advantage (2011), Why The Rich Are Getting Richer – What is financial education (2017) and More Important Than Money (2017).

Tom's Blog Posts (270+ Posts)

How Soon Should You Form Your Entities?

A Good Investor Requires a Tax Strategy

9 Deductions for Your Vacation Properties

How to turn ordinary income into passive income

Did You Leave Money on the Table This Tax Season?

3 Deductions You Probably Missed

5 Legal Deductions for Entrepreneurs

How To Pay No Taxes With Real Estate

How To Create Tax-Free Wealth

International Speaker

Wheelwright is a global speaker on tax and wealth strategies for small businesses and investors. Since 2011, Wheelwright has been a keynote speaker at Rich Dad conferences worldwide on six continents (Africa, Asia, Australia, Europe, North America, and South America) with Robert Kiyosaki (Author, “Rich Dad Poor Dad”).

In his presentations, Wheelwright stressed his belief that, “The tax laws in every country are first and foremost a series of incentives for business owners and investors and reflect that country’s policies towards energy and economic development.”

Events

Tom's Company

In 2017, interest in Tom's approach to tax reduction and wealth building became so great that Tom needed more than 1 CPA firm to properly serve each client.

So Tom sold his CPA firm and created an education company: WealthAbility® with the mission to educate more entrepreneurs and investors than ever before. To service those customers, Tom premiered the WealthAbility® Network of tax professionals trained and certified in Tom's concepts and practices.

Media & Interviews

How Debt & Taxes Can Make You Rich (Cheddar)

Book Release with Rich Dad Advisors on Fox

5 Most Overlooked Tax Deductions

How to Deduct Your Family Vacation

Tom's Podcast

In The WealthAbility Show, Tom Wheelwright guides entrepreneurs and investors into a revolutionary approach to thinking about taxes and wealth-building. Tom is an unapologetic proponent of the radical idea that you are fully capable of controlling your own financial future. And that you–not Wall Street–have a God-given right to control your money, build your wealth, and achieve your financial dream.

Are you a CPA or Tax Professional?

Take some time to learn about Tom's Tax Professional network.